TLDR:

- Cross-border finance still operates on systems built in the 1970s. These are slow, expensive, and fragmented

- Stablecoins, digital assets backed by fiat currencies, represent a generational opportunity to rebuild these rails from the ground up

- Opportunities stretch from B2B (treasury management, invoice payment) to B2C (payroll, prosumer payout) to C2C (remittance), where stablecoins can provide an operating system for a more seamless movement of money

Money is the largest market in the world, yet the rails that it relies on are painfully outdated.

The $200 trillion cross-border payments market primarily runs on correspondent banking networks built in the 1970s, and has barely changed since. These rails are slow, expensive, and opaque, requiring multiple intermediaries to complete a single transaction.

Settlement often takes days, and costs accumulate at every step in the chain. Attempts at modernization over the past decade (liquidity pools, API layers) have only wrapped new technology around old infrastructure without solving the problems at its core.

Today, we’re at an inflection point. Blockchain-based settlement has reached escape velocity, offering the first credible alternative to SWIFT. This momentum is supported by trillions in annual stablecoin flows, growing regulatory clarity (the US GENIUS Act, the EU’s MiCA regulation), and integration by household financial names like Visa, Mastercard, and JPMorgan.

We believe this rise of stablecoin infrastructure marks a once-in-a-generation shift in how money moves globally.

Stablecoins: a step change for global finance

Stablecoins are digital assets pegged to fiat currencies, designed to combine the stability of government-issued money with the programmability of blockchain technology. At their core, they act as a neutral settlement layer, enabling value to flow across borders instantly, at minimal cost, 24/7. In short, stablecoins make money move like data – programmable, modular, and interoperable.

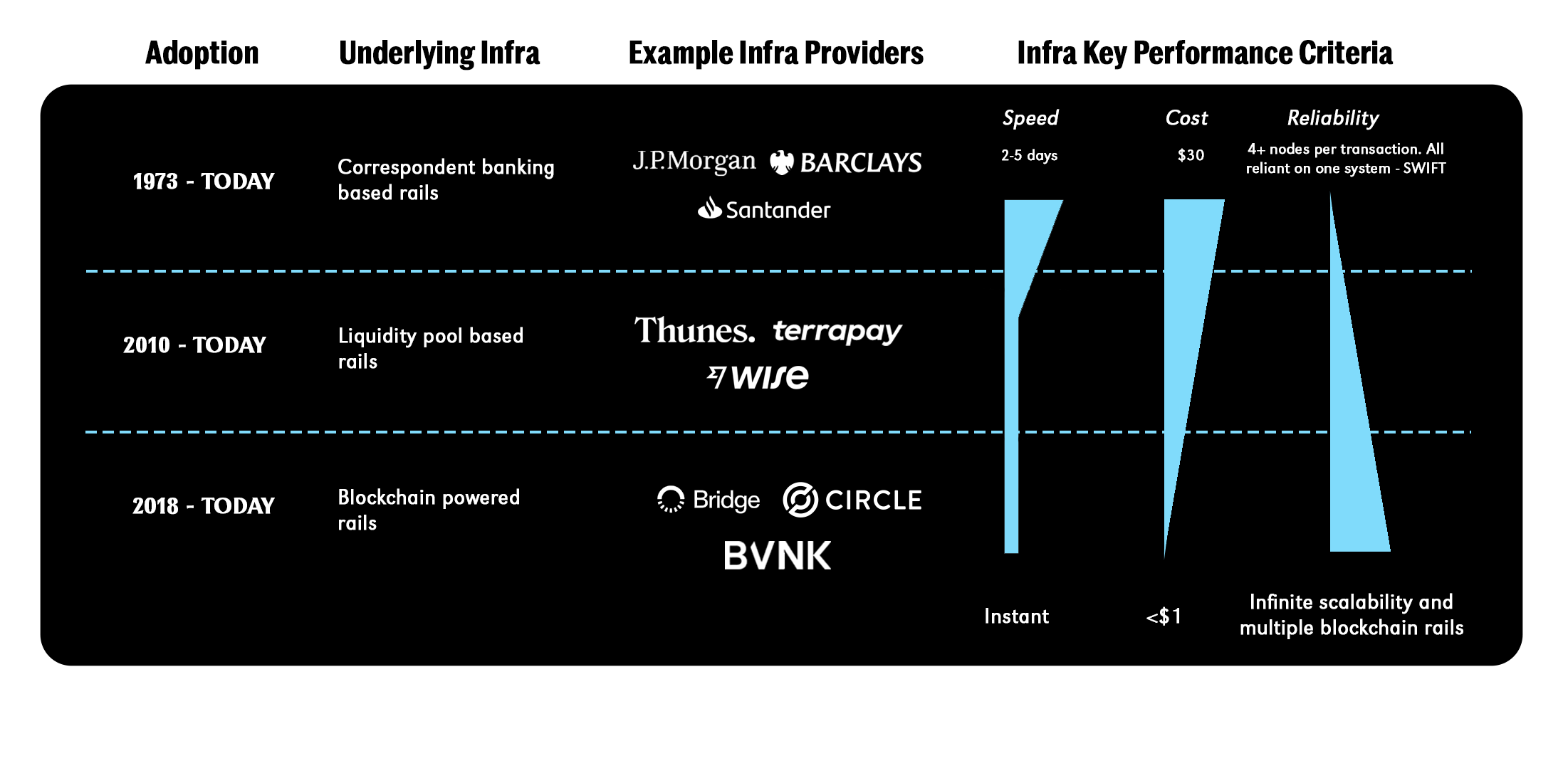

To grasp why stablecoins matter, it’s helpful to trace the evolution of payment rails.

In the 1970s, correspondent banking created the first global standard for cross-border transfers, but relied on a patchwork of closed systems and intermediaries. The 2010s brought liquidity-pool models, which simulated real-time settlement by pre-funding local accounts, though they remained tied to the heavy capital requirements of traditional finance.

Since 2018, blockchain rails have introduced a step change: enabling near-instant settlement, significantly lower transaction costs, and effectively unlimited scalability. Stablecoins anchor this new era, serving as the bridge between legacy finance and digital-native systems.

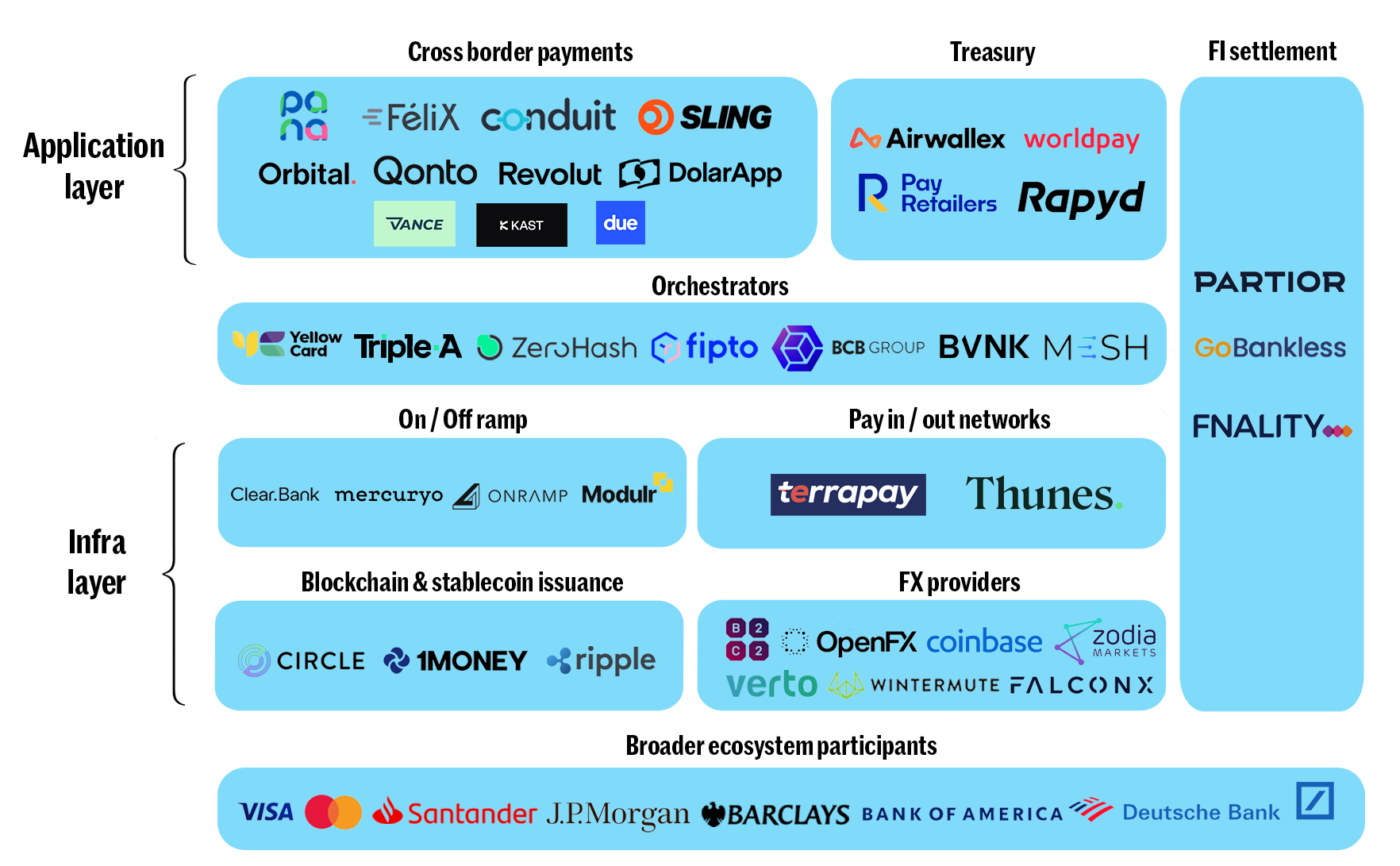

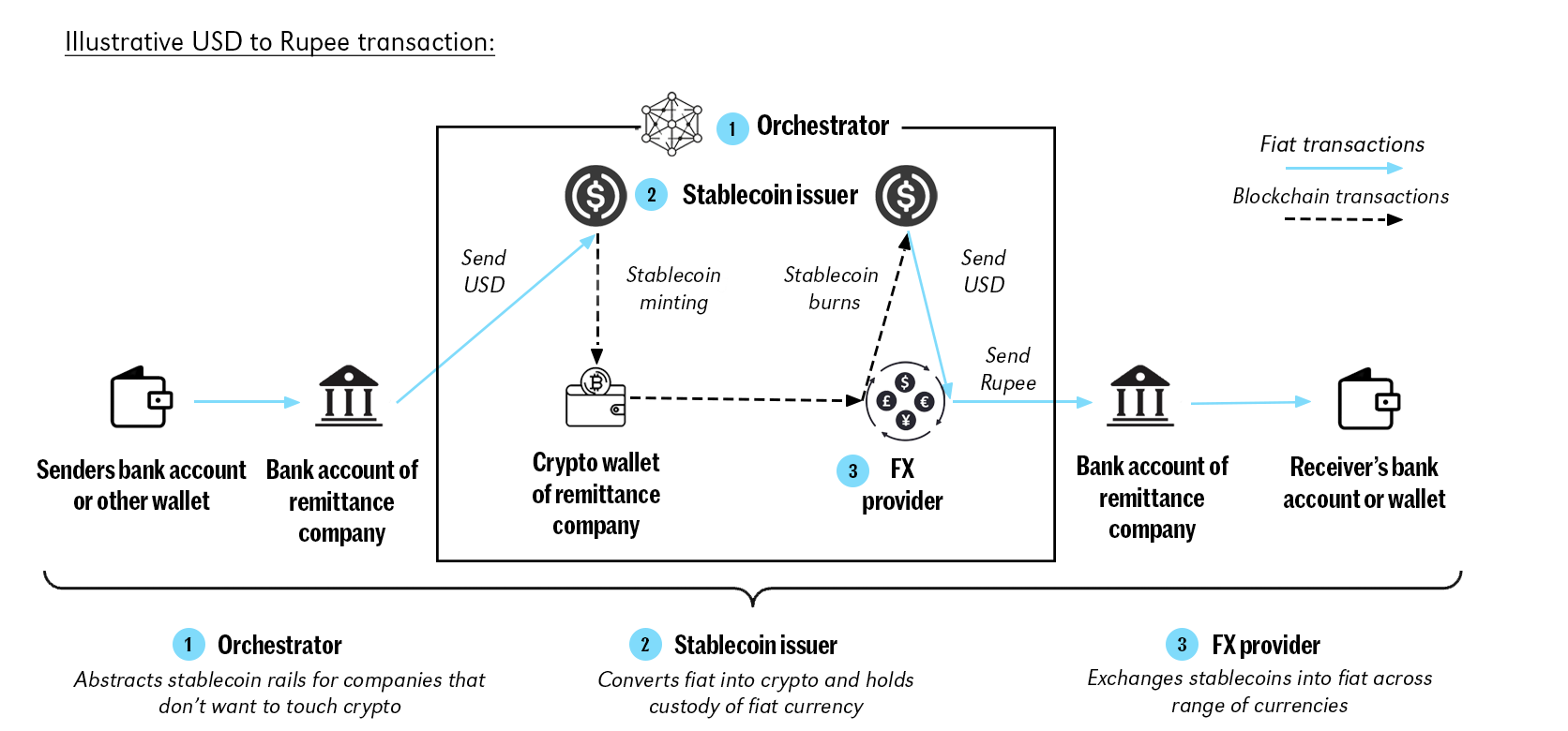

The stablecoin stack is coming together at remarkable speed. At its foundation are the issuers, responsible for minting and redeeming tokens backed by fiat reserves. Built on top are FX providers and liquidity orchestrators, transforming the messy mechanics of conversion and settlement into a seamless interface. Above them sits the application layer – remittance firms, PSPs, payroll platforms, and neobanks – that weave stablecoins into everyday financial services.

Taken together, these layers form a new operating system for money (see below), with stablecoins serving as the connective tissue that links banks, blockchains, and end users into a seamless network.

The scale of the stablecoin opportunity

Stablecoins’ potential is hard to overstate.

Global cross-border payments incur hundreds of billions in fees, spreads, and friction each year. Beyond the direct costs, vast amounts of working capital sit idle in transit, liquidity that could otherwise be put to productive use across the economy.

Stablecoins address these pain points head-on: they strip out intermediaries, reduce the need for costly pre-funding, and enable settlement that is not just faster but instantaneous and around the clock.

Crucially, adoption is no longer theoretical. Stablecoin transaction volume reached $27 trillion last year, rivaling major card networks and demonstrating undeniable product-market fit.

Much like the internet rewired communications and cloud computing rewrote IT, stablecoins are now rewriting the underlying code of global finance—forcing banks, fintechs, and enterprises to adapt to a system that moves at the speed of software, not paper.

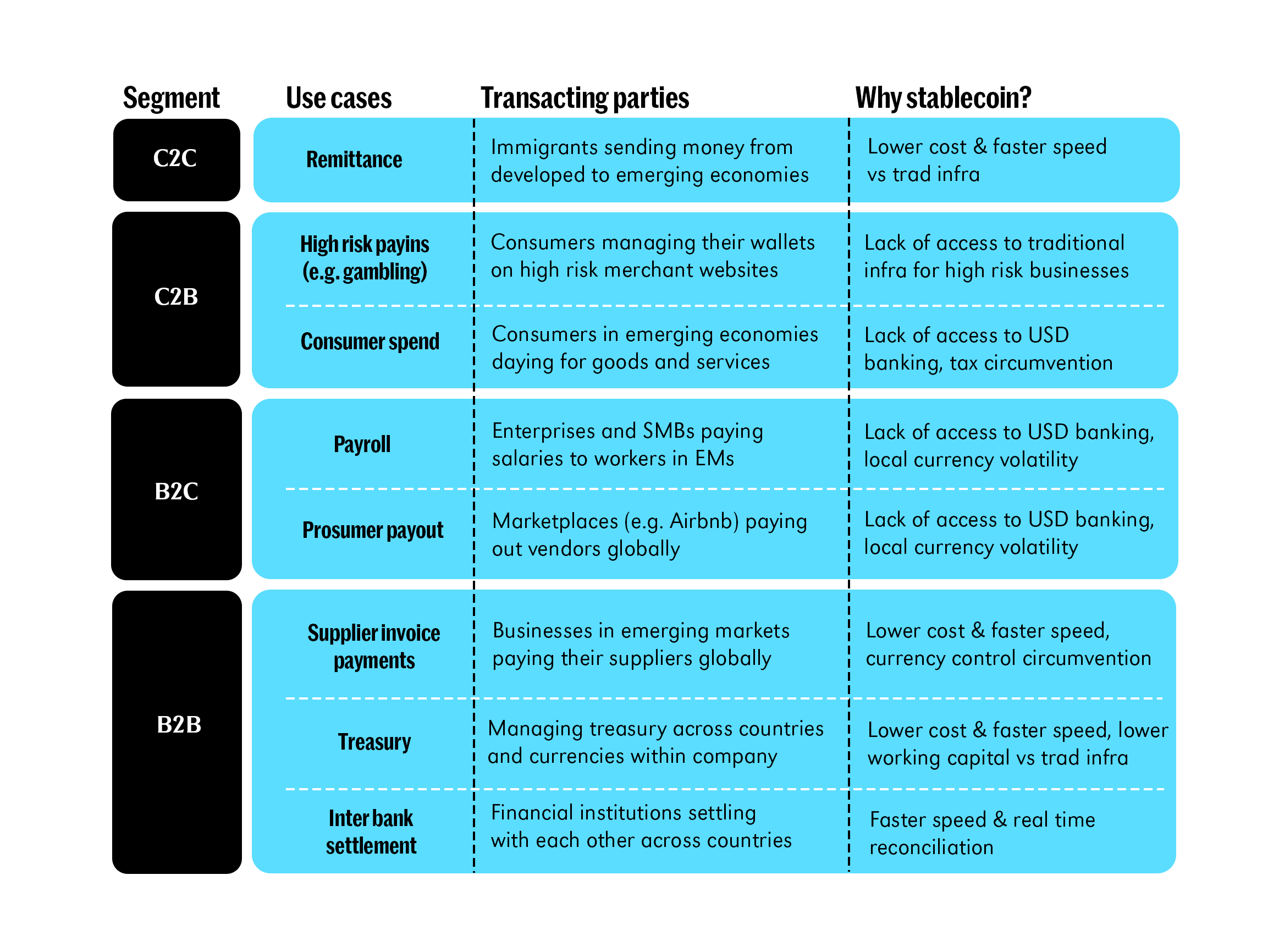

From B2B to B2C: Where we’re seeing pull already

Adoption across the value chain is being accelerated by segments where traditional infrastructure is weakest and pain points are most acute: crucially, where stablecoins are adopted not as an alternative currency but as a better technology for money movement.

Remittances are an obvious entry point: migrant workers sending money home have long endured fees of 5-10% and multi-day settlement windows; stablecoins reduce that to near-zero fees and instant settlement, in a form that is widely accessible via mobile wallets, bypassing restrictive banking systems in emerging markets.

In B2C use cases, payroll and prosumer payouts stand out. Startups and SMEs operating globally can now pay contractors or employees in stablecoins, circumventing the costs and volatility of local systems. Marketplaces such as Airbnb and Etsy have begun exploring payouts in stablecoins, which are particularly valuable in emerging markets where dollar accounts are otherwise inaccessible.

On the B2B side, supplier invoice payments and treasury management are emerging as early proving grounds. Businesses in emerging markets are turning to stablecoins to pay international suppliers, while multinational companies are also experimenting with stablecoin-based treasury flows to move funds between subsidiaries and across borders in real time. By reducing the need for pre-funded accounts, these systems free up working capital that can be redeployed into growth.

Finally, financial institutions themselves are beginning to adopt stablecoins for interbank settlement, using them as a 24/7 bridge currency for reconciliation across jurisdictions to improve liquidity management and reduce risk.

Looking Ahead

At Northzone, we’ve spent a long time thinking about the future of money movement – one of the most significant and enduring profit pools in finance. Every so often, we’d meet brilliant teams trying to modernize parts of the system, but the legacy infrastructure still constrained most of them.

That started to change when stablecoins emerged as a genuine technology unlock, a way to rebuild global finance from first principles. Over the last 18 months, we’ve met dozens of founders building across the stack: some reimagining settlement, others tackling compliance, treasury, or connectivity across markets.

The best founders share a common mindset. They’re focused on real-economy use cases and are solving deep, structural problems in how money flows. They understand where the old system breaks, and are designing something fundamentally more efficient, transparent, and interoperable in its place.

Stablecoins have now matured beyond a fringe crypto experiment; they are already proving themselves as critical plumbing for global finance. Settlement volumes are in the trillions, regulators from the US to Europe to Singapore are putting frameworks in place, and enterprises are beginning to integrate stablecoin rails into real payment flows.

As stablecoins move from proof-of-concept to scale, the challenge shifts from innovation to integration. The winners will be those building the infrastructure that connects stablecoins seamlessly into the global financial system: from compliant on- and off-ramps to enterprise-grade treasury and settlement tools to the FX and liquidity layer. These are the systems that will make stablecoins a default part of how money moves.

It’s important to stress how early we still are. The map of players today is only a snapshot of a market in motion. New companies are launching every week to plug liquidity gaps, build faster payout networks, or develop applications that integrate stablecoins into existing financial workflows. This is what makes the space so dynamic: the rails are being laid even as demand is pulling them forward.

If you’re one of those founders shaping the next generation of financial rails, we’d love to hear from you: sanjot@northzone.com, manavi@northzone.com, alex@northzone.com